As an ecosystem, we spend large amounts of time obsessing over cash burn, runway and financing at startups.

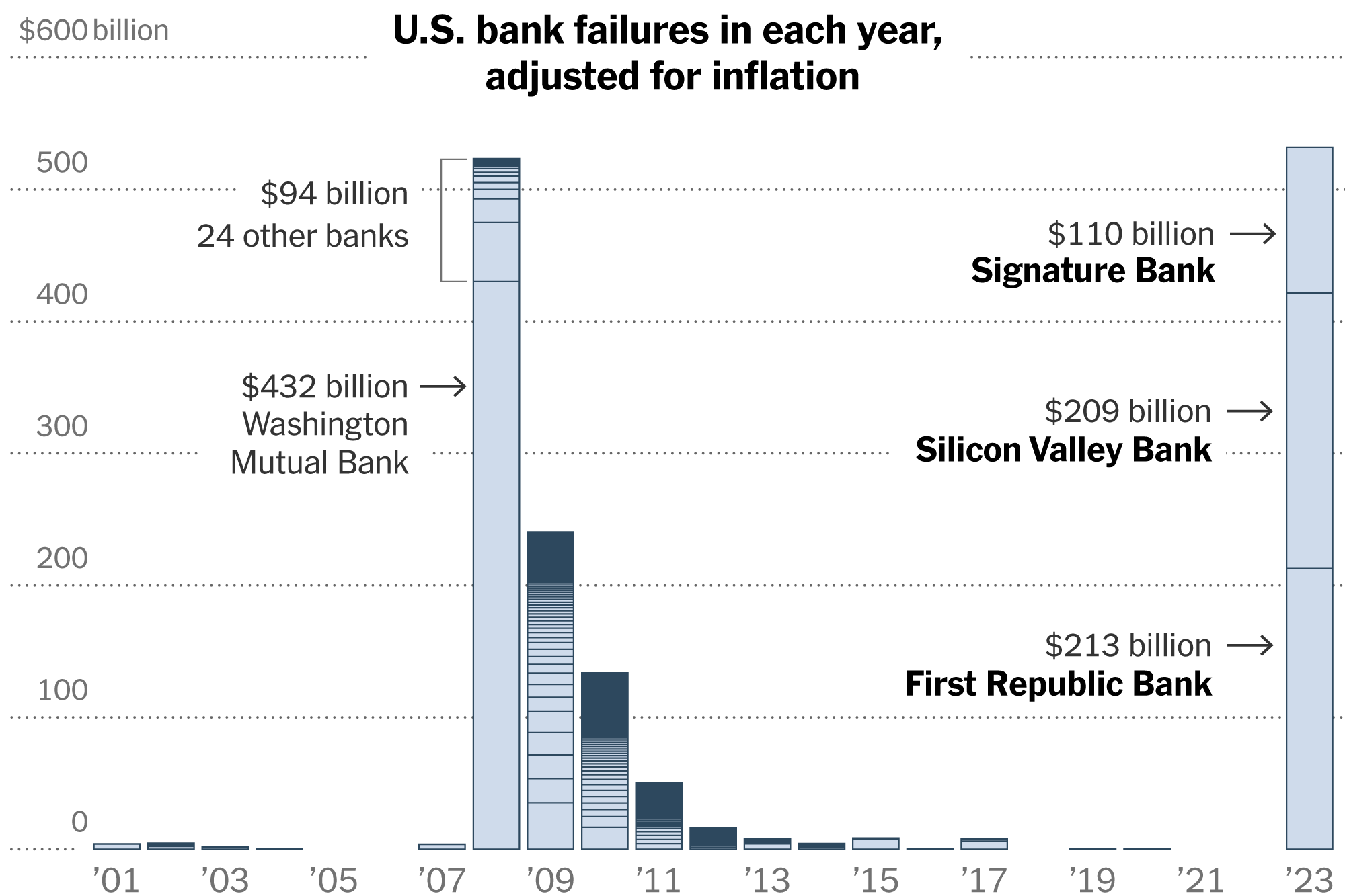

It has become clear 2023, in the wake of the collapse of both Silicon Valley Bank and First Republic Bank, that founders and CFOs also need to have a salient strategy for cash management and protection.

We’re being asked by founders about how they should:

- Manage security of funds across banking providers;

- Ensure they have access & liquidity of funds; and

- Optimise interest rates and protection against inflation.

We have collaborated with Primary to build this guide to help founders develop secure cash management strategies, with these priorities in mind:

- Eliminating the single point of failure in banking relationships

- Developing an understanding of how much cash sits at each level of your treasury

- Putting idle cash to work, protecting against inflation

- Spotting fraud threats and minimising them.

We’ll highlight why each steps is important and how to turn them into action.

Why do old approaches no longer cut it?

The failure of SVB and First Republic show banks are not immune to failure

The current macroeconomic uncertainty is threatening our startup ecosystem. Early stage companies are being asked to rest their fate on the stability of third-party ecosystem providers, like banks and payment companies.

We’ve seen the impact of bank failures overseas: a third of startups who banked with Silicon Valley Bank had no access to alternative banking facilities at the time of collapse. While we are pleased that depositors were ultimately able to recover their funds, we are uncomfortable with the idea that companies needed to rely on a regulator to bail out banks to save their business deposits.

These events have thrust the unfamiliar area of cash security and management into the spotlight for founders around the world.

While the Australian banking landscape presents lower risk, it is still wise to exercise caution

As the banking crisis continues in the U.S., we are speaking to Australian founders, CFOs and financial controllers who remain uncertain about what they should be doing with their cash.

Our assessment of the banking environment in Australia is that the risk of a big four bank suffering a collapse is very small. National Australia Bank (NAB), Australia and New Zealand Bank (ANZ), Westpac, and the Commonwealth Bank of Australia (CBA) are classed as domestic systematically important banks (D-SIBs) in Australia. This means that Australian regulators have identified each of these institutions as systematically important to the health of the economy and are ‘too big to fail’ from a domestic perspective.

Whilst Australia's big four banks are not recognised as global systematically important banks (G-SIBs) and therefore not automatically bailed out by foreign governments, Australian banks are amongst the best capitalised in the world and the risk of a government default in Australia is extremely low.

The more likely risk relates to access to underlying payment infrastructure. Individual banks have a history of technological issues that can restrict access to money movement. Only last year did we see one of the big four experience payment network reliability issues. Access problems can restrict the ability to move quickly, so spreading cash across multiple accounts is important to create redundancy.

While we are largely comfortable with the safety that our D-SIBs offer, we recommend that you do not have a single point of failure.

Thanks for reading AfterWork Reading! Subscribe for free to receive new posts and support our work.

Subscribe

Guidelines for founders developing a cash management strategy

1. Eliminate the single point of failure

Startups can reduce their concentration risk by opening accounts with multiple banks. Having relationships with 2-3 separate trusted banking institutions with money distributed across accounts is best practice. The banks we recommend in Australia are:

- NAB;

- ANZ;

- Westpac;

- Commonwealth Bank of Australia.

Where your funds are held by a non-bank entity (like a payment provider), you should understand who banks the provider and what happens to your funds in the event of an issue with the provider.

Accounts across all institutions should be dedicated to specific functions (i.e. payroll, expenses) and you should be keeping up-to-date visibility of the balances in these accounts. Setting up purpose-built accounts will mean that you’ll have extra control over the funds in an emergency. Since you know where all funds sit at all times, you can also rapidly move your money in the instance that you face issues with one particular provider.

For businesses with expansion plans or multiple global entities, we also recommend considering establishing relationships with global systematically important banks:

- Bank of America;

- Bank of New York Mellon;

- Citigroup;

- Goldman Sachs;

- JP Morgan;

- Morgan Stanley;

- HSBC.

For management of funds across borders, you should consider splitting funds across more than one bank. If you don’t make a timely FX transfer, or your international provider freezes your funds, you run the risk of missing deadlines like payroll. In the case that you have operational expenses in different jurisdictions, you should treat these international accounts the same as your local accounts.

2. Understand how much cash sits at each level of your treasury

Your treasury consists of three levels:

- Cash: 6 months worth of expenses maintained across 2-3 operating bank accounts with tier- one banks.

- Short-term: Idle cash that is not required for at least 6 months; to be invested in secure, liquid options to extend runway and protect against inflation.

- Strategic: Well-capitalised startups (Series B & beyond) should seek bespoke investment options to further diversify risk and improve returns on longer term idle cash.

If founders can clearly articulate how funds are distributed across these levels, they will increase investor confidence in their cash management practices.

To apply this to your business, we encourage you to calculate your burn and requirements of operating cash to understand how much you need to keep as cash on hand. Once you’ve accounted for this level, you can then use the following points to decide how you allocate capital across short term & strategic.

3. Use your idle cash to protect against inflation

There is an estimated $100 billion earning little to no interest in Australian business bank accounts. With inflation at the highest levels in a decade, businesses with multi-year runways are at risk of letting this money erode away.

As a starting point, we recommend you speak to your existing banks to understand what safe, high interest rate products they offer. Some popular options for short-term cash allocation are rolling term deposits (e.g. 3 months, with option to break) and cash ETFs. You can also sweep excess funds into higher interest accounts & funds on a daily basis to maximise interest.

For more mature businesses that need to consider strategic investments, we encourage you to collaborate with your investors & advisors to design a policy that sets out how you’re planning to protect your funds from inflation. Options include longer duration term deposits and fixed income portfolios. They will help you build a treasury framework and introduce you to external providers.

The bottom line is: be sensible about the instruments you invest in and double check with your investors if you have any concerns. Your goal is to ensure you are protecting cash from inflation and opportunity cost without taking on unnecessary risk. To find the best options for you, lean on your investors, treasury consultants like Rochford Capital & Azzana or treasury management operating systems like Primary.

4. Spot fraud threats and minimise them

Phishing attacks pose an enormous risk for startups, particularly those with multiple bank partnerships and accounts.

On one side, approval flows and processes are critical for meaningful money movements. You should clearly define what constitutes a large transaction, who the relevant approving parties are and what information needs to be shared. We recommend that founders adopt the four eyes principle of approvals to mandate rules around payment instructions. If there are changes to these instructions (i.e. a vendor changes the bank account they ask you to pay into), you should verify them through multiple channels.

On the other side, it is important to educate and continually remind your teams of threats. Ensure that essential cyber security protection and training is in place. You can create your own training practices using this comprehensive guide to startup security, or use a tool like SafeStack to help design the process for you.

Where to go for more information

Primary, the modern operating system for treasury management

Treasury management consultants including Azzana and Rochford Capital

Macquarie Asset Management

This guide is endorsed by these firms.

Disclaimers:

[1] The information in the guide is intended to be general in nature and is not financial product advice. It does not take into account your business objectives, financial situation or needs. Before acting on any information, you should consider the appropriateness of the information provided and the nature of the relevant financial product having regard to your objectives, financial situation and needs.

[2] The links shown are being provided as a convenience and for informational purposes only; they do not constitute an endorsement or an approval by the undersigned of any of the products, services or opinions of the corporation or organization or individual.